Nexo Dual Card Review 2026

Dual-mode Mastercard: Credit mode borrows against crypto (1.9-13.9% APR by tier), Debit mode spends fiat/stablecoins/FiatX at up to 14% APY. Up to 2% NEXO cashback with $5,000+ balance. EEA, UK, and Switzerland.

SpendNode Rating

Nexo still feels built around convenience first. The hybrid structure is the whole point, so that has to carry the rating.

Credit mode or debit mode, one card. That hybrid is the pitch and, honestly, it works for people who want flexibility without managing two products. 4.0 on Product Utility reflects that. The 3.3 on Custody and Trust is the other side: your assets live on Nexo. After 2022, that sentence carries more weight than it used to.

How It Competes

Cost Efficiency

3.9

Product Utility

4.0

Custody & Trust

3.3

Reliability & UX

3.9

Transparency

3.7

CASHBACK

Verified

VIRTUAL CARD

Verified

NO ANNUAL FEE

Verified

Our Official Verdict

Hybrid Spend Mastery: 2% Rewards + Up to 14% APY Balance

The Nexo Dual Card is the benchmark for crypto-backed credit. By maintaining a Free annual fee and offering 2% cashback, it serves as a powerful off-ramp that preserves your long-term portfolio growth.

Fees & Charges

Annual Fee

Free

FX Fee

0.2%

ATM Fee

2%

Requirements

Supported Regions

EEA, UK

Spendable Assets

NEXO, BTC, ETH, USDT, USDC, EURx, USDx, GBPx

Nexo Dual Card Review

The Nexo Dual Card is a hybrid Mastercard available in the EEA, UK, and Switzerland that toggles between Debit mode (spend fiat, stablecoins, or FiatX while earning up to 14% APY paid daily on idle balances) and Credit mode (borrow against crypto collateral at 1.9-13.9% APR depending on loyalty tier), offering 0.5-2% cashback in NEXO tokens or 0.1-0.5% in BTC in Credit mode only, with a mandatory $5,000 minimum account balance for any cashback.

One Card, Two Modes, No Selling Required

Every other crypto card forces a binary choice: sell your crypto to spend (debit) or lock it up and borrow against it (credit). The Nexo Dual Card eliminates this choice with an in-app toggle that switches spending modes transaction by transaction.

Credit mode: Nexo uses your crypto portfolio as collateral to open an instant credit line. APR ranges from 1.9% (Platinum, LTV below 20%) to 13.9% (Base). Your BTC, ETH, and other assets remain in your portfolio - no selling, no taxable event.

Debit mode: You spend your EUR, GBP, stablecoin, or FiatX (EURx, USDx, GBPx) balance directly. Drag-and-drop asset priority lets you choose which assets get spent first. Up to 14% APY on idle funds, paid daily (rate depends on loyalty tier and asset), but no card cashback is paid in Debit mode.

The toggle is instant. No other card in the market offers this level of spending flexibility.

SpendNode app screenshot

Nexo Dual Card - Up to 2% cashback in Credit mode, Apple Pay and Google Pay, instant Credit/Debit toggle, and no minimum repayments or inactivity fees. Requires $5,000+ balance for cashback.

Important qualifier: Cashback on all purchases requires a minimum $5,000 account balance in digital assets. Below $5,000, you earn 0% cashback regardless of tier.

Card Specs

Physical and Virtual

- Virtual card: Instant activation with $50 minimum balance

- Physical card: Ordering paused since January 17, 2025. When available, requires $5,000+ balance and Gold tier minimum

- Card currency: EUR or GBP, chosen once at activation (cannot be changed)

- Network: Mastercard

- Mobile wallets: Apple Pay, Google Pay

- Contactless: Yes (NFC)

- Both modes: The same card operates in credit or debit mode depending on your toggle setting

Security

- 2FA: Biometric and PIN authentication in the Nexo app

- Instant freeze/unfreeze: Toggle card on/off in-app

- Real-time notifications: Push alerts for every transaction

- Insurance: Custodial assets insured via BitGo and Ledger Vault

- SOC 2 compliance: Nexo has achieved SOC 2 Type II certification

- Cold storage: Majority of assets held in institutional-grade cold storage

How Spending Works: Transaction Flow

Credit Mode Example: EUR 2,000 Designer Purchase in Milan

Step 1: Check your credit line

- You hold $20,000 in BTC on Nexo

- At 50% LTV (loan-to-value), your available credit line is $10,000

- At Platinum tier, APR on your credit line is 1.9% (Low-Cost rate, LTV below 20%)

Step 2: Toggle to Credit mode

- In the Nexo app, set your card to "Credit" mode

- No transfer, no conversion, no setup needed

Step 3: Pay at the store

- Tap your Nexo card. EUR 2,000 is charged

- Nexo extends a credit line of EUR 2,000 against your BTC collateral

- Your BTC stays in your portfolio (unreduced, unsold)

- FX fee: 0.2% (weekday, EEA) = EUR 4.00

Step 4: Cashback credited

- At Platinum: 2% x EUR 2,000 = EUR 40 in NEXO tokens (requires $5,000+ balance)

Step 5: Repay at your pace

- The EUR 2,000 credit line accrues interest at 1.9% APR (Platinum with LTV below 20%)

- Annual interest cost on EUR 2,000: approx. EUR 38

- Repay from any asset on Nexo, or from fiat

- Crypto repayment fee: 0.26% flat fee (stablecoin repayments have no fee)

- If BTC drops significantly and LTV exceeds the safe threshold, Nexo issues a margin call

Tax efficiency: In many jurisdictions, borrowing against crypto is not a taxable event - unlike selling crypto to fund a debit card. Credit mode can defer capital gains until you actually sell. Consult your tax advisor.

Debit Mode Example: EUR 50 Grocery Purchase

- Toggle to "Debit" mode

- Have EUR or stablecoins in your Nexo account

- Tap your card. EUR 50 is deducted from your balance

- Cashback: 0.5-2% in NEXO tokens depending on tier (requires $5,000+ balance)

- Idle balance continues earning up to 14% APY, paid daily

The Loyalty Tier System

Your Credit mode reward rate, Credit mode APR, and ATM allowance depend on how much NEXO you hold as a percentage of your total portfolio on the platform:

| Tier | NEXO Required | Cashback (NEXO) | Cashback (BTC) | Credit APR | ATM Free Limit |

|---|---|---|---|---|---|

| Base | None | 0.5% | 0.1% | 13.9% | EUR 200/mo |

| Silver | 1% of portfolio | 0.7% | 0.2% | 6.9% | EUR 400/mo |

| Gold | 5% of portfolio | 1.0% | 0.3% | 3.9% | EUR 1,000/mo |

| Platinum | 10% of portfolio | 2.0% | 0.5% | 1.9% | EUR 2,000/mo |

Low-Cost Credit rates (Gold 3.9%, Platinum 1.9%) require your Credit Wallet LTV to stay below 20%. Above 20% LTV, standard (higher) rates apply.

$5,000 minimum: Cashback is only earned when your account balance exceeds $5,000 in digital assets. Below this threshold, you receive 0% cashback at all tiers.

Platinum Tier Economics

To reach Platinum, 10% of your Nexo portfolio must be in NEXO tokens:

| Total Portfolio | NEXO Required (10%) | Approx. NEXO Cost |

|---|---|---|

| $10,000 | $1,000 in NEXO | $1,000 |

| $50,000 | $5,000 in NEXO | $5,000 |

| $100,000 | $10,000 in NEXO | $10,000 |

Key difference from Crypto.com: Nexo requires a percentage of your existing portfolio in NEXO tokens. There is no fixed dollar lockup and no lockup period. You can sell NEXO at any time (though this would downgrade your tier). Crypto.com requires a fixed dollar amount locked for 12 months.

Fee Deep Dive: The Real Cost

Foreign Exchange Fees

FX fees apply to all tiers equally - there is no tier-based reduction:

| Region | Weekday FX | Weekend FX |

|---|---|---|

| EEA / UK / Switzerland | 0.2% | 0.7% |

| Rest of World | 2.0% | 2.5% |

On top of Nexo's FX fee, the Mastercard network applies its own spread (typically 0.2-0.4% vs interbank), making the effective total markup 0.4-1.1% for EEA transactions.

Credit Mode True Cost Analysis

The real cost of Credit mode depends entirely on your tier. Assumes $5,000+ balance for cashback, EUR 3,000/month spend, and Low-Cost APR rates (LTV below 20%):

| Tier | Annual Spend | Credit APR Cost | Cashback Earned | Net Position |

|---|---|---|---|---|

| Base (13.9%) | EUR 36,000 | -EUR 5,004 | +EUR 180 (0.5%) | -EUR 4,824 |

| Silver (6.9%) | EUR 36,000 | -EUR 2,484 | +EUR 252 (0.7%) | -EUR 2,232 |

| Gold (3.9%) | EUR 36,000 | -EUR 1,404 | +EUR 360 (1.0%) | -EUR 1,044 |

| Platinum (1.9%) | EUR 36,000 | -EUR 684 | +EUR 720 (2.0%) | +EUR 36 |

Critical insight: Credit mode barely breaks even at Platinum (1.9% APR) and loses money at every other tier. If you cannot reach Platinum, use Debit mode or choose a different card. Gold at 3.9% APR costs EUR 1,044/year more than the cashback earns.

ATM Withdrawals

Free ATM allowance is amount-based (not count-based):

| Tier | Free Monthly Limit | Over-Limit Fee |

|---|---|---|

| Base | EUR 200 / GBP 180 | 2% (min EUR/GBP 1.99) |

| Silver | EUR 400 / GBP 360 | 2% (min EUR/GBP 1.99) |

| Gold | EUR 1,000 / GBP 900 | 2% (min EUR/GBP 1.99) |

| Platinum | EUR 2,000 / GBP 1,800 | 2% (min EUR/GBP 1.99) |

Loan Repayment Fees

Credit mode purchases generate loans in xUSD. When repaying with crypto (excluding stablecoins and FIATx), a 0.26% flat fee applies. Stablecoin repayments have no fee.

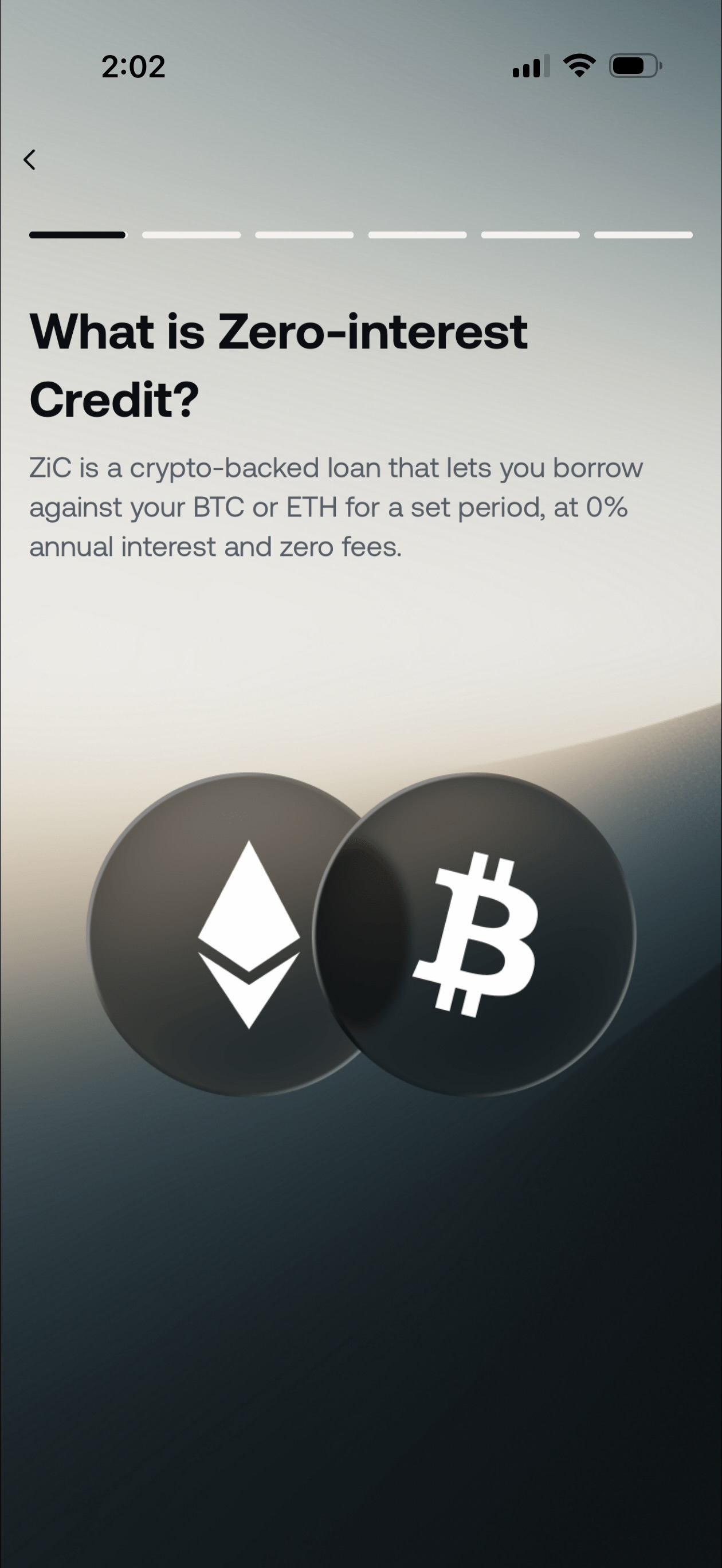

Zero-Interest Credit (ZiC): A Separate Structured Product

Nexo also offers Zero-Interest Credit (ZiC), a borrowing feature confirmed by in-app screenshots. ZiC is NOT the standard Credit mode APR - it is a separate structured product with specific terms:

SpendNode app screenshot

Zero-Interest Credit (ZiC) - Borrow against BTC or ETH for a set period at 0% interest and zero fees. Fixed duration (not open-ended like standard credit). The "set period" is key.

- 0% interest, 0% fees on borrowed amount

- BTC and ETH collateral only

- Fixed duration (not open-ended like standard credit)

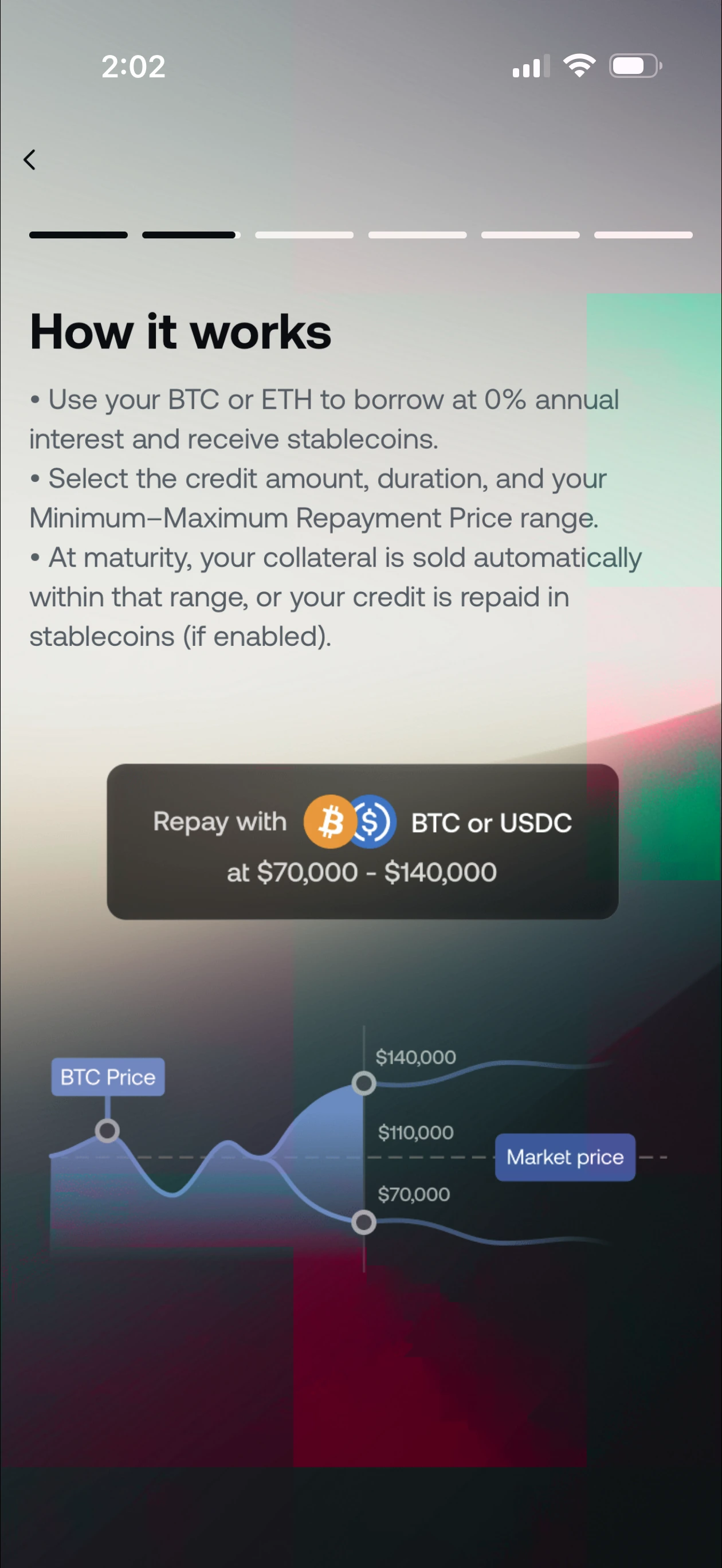

- Min-Max Repayment Price range - you set a floor and ceiling for your collateral price at maturity

- Below minimum: Your collateral settles at the floor price (downside protection for you)

- Above maximum: Your collateral settles at the ceiling price (you give up upside above the cap)

- Repay with BTC or USDC at maturity

SpendNode app screenshot

The Collar Mechanism - Set a $70K-$140K BTC price range. Below $70K: downside protection. Above $140K: upside capped. This is the trade-off for 0% interest - you are selling volatility.

ZiC is essentially a collar strategy. The "cost" of 0% interest is capping your BTC/ETH upside. If BTC rallies 100% during your ZiC term, you only benefit up to your maximum repayment price. This is a meaningful trade-off for long-term holders.

ZiC vs Standard Credit Mode:

| Feature | Standard Credit Mode | ZiC |

|---|---|---|

| APR | 1.9-13.9% by tier | 0% |

| Duration | Open-ended | Fixed term |

| Collateral | 40+ crypto assets | BTC and ETH only |

| Upside cap | None (you keep all upside) | Yes (capped at max price) |

| Downside protection | None (full margin risk) | Yes (settles at floor) |

| Availability | All tiers | Separate feature |

Example: Borrow $50,000 against BTC via ZiC

- You set a min repayment price of $80,000 and max of $120,000 (current BTC: $95,000)

- If BTC drops to $70,000 at maturity: your collateral settles at $80,000 (you are protected)

- If BTC rises to $150,000 at maturity: your collateral settles at $120,000 (you gave up $30,000 in upside)

- If BTC stays between $80,000-$120,000: you repay normally and keep your BTC

Technology: The Dual-Mode Engine

Nexo's card is powered by its lending platform, operational since 2018:

- Instant toggle: Switch between Credit and Debit in the Nexo app

- Credit mode settlement: When you tap, Nexo instantly opens a micro-loan against your crypto, converts to fiat, and pays the merchant. Interest accrues from the moment of purchase

- Debit mode settlement: Standard fiat spending from your EUR/GBP/stablecoin/FiatX balance with drag-and-drop asset priority

- Supported spending assets: NEXO, BTC, ETH, USDT, USDC, EURx, USDx, GBPx

- Collateral assets (Credit mode): 40+ cryptocurrencies accepted

- Apple Pay / Google Pay: Both supported

- 3D Secure: Push notification verification for online purchases

Up to 14% APY on idle debit balances (paid daily, depending on loyalty tier and asset type) positions Nexo among the highest-yielding card accounts in the market.

Real User Scenarios

Scenario 1: Henrik (HODLer, EUR 4,000/month, Credit Mode)

Setup:

- Nexo Dual Card in Credit Mode

- $80,000 BTC portfolio on Nexo (50% LTV = $40,000 credit line)

- Platinum tier (10% portfolio in NEXO = $8,000 in NEXO)

- $5,000+ balance - qualifies for cashback

- Uses credit line for all spending (no selling BTC)

Monthly math:

- Rewards: EUR 4,000 x 2% = EUR 80 in NEXO

- Credit APR cost: EUR 4,000 x 1.9% / 12 = -EUR 6.33 (assuming prompt monthly repayment)

- FX fees (30% international, weekday): EUR 1,200 x 0.2% = -EUR 2.40

- Net monthly value: EUR 71.27

- Annual: EUR 855

- Tax savings: Avoids capital gains on EUR 4,000/month in BTC sales (potentially thousands in high-tax jurisdictions)

His verdict: "The tax efficiency is the real value. In Germany, selling BTC within a year triggers 26% capital gains tax. Credit mode lets me spend without selling. On EUR 48,000/year in spending, I defer thousands in potential taxes. The 2% NEXO rewards are a bonus, but the 1.9% APR eats into them - I net about EUR 36 from cashback minus interest alone. The tax deferral is what makes this card worth it."

Risk: His $8,000 in NEXO tokens could lose 50%, wiping out EUR 4,000. The credit line exposes his BTC to liquidation if markets crash 40%+.

Scenario 2: Marie (Conservative, EUR 2,000/month, Debit Mode)

Setup:

- Nexo Dual Card in Debit Mode

- EUR 15,000 balance earning up to 14% APY (rate varies by tier and asset)

- Silver tier (1% NEXO = modest holding)

- $5,000+ balance - qualifies for cashback

- Purely domestic EEA spending

Monthly math:

- Rewards: EUR 2,000 x 0.7% = EUR 14 in NEXO

- APY on EUR 15K: varies by tier and asset (significantly higher than traditional savings; up to EUR 175/month at Platinum rate on eligible assets)

- FX fees: EUR 0 (domestic only)

- Net monthly value: EUR 14 cashback + yield on idle balance = well above traditional card returns

Her verdict: "I use Debit mode exclusively. The daily yield on my idle balance is the whole point here because Debit mode does not pay cashback. I keep a small NEXO position for Silver tier but would not go higher - too much token risk for a product I mainly use as a yield-bearing spending balance."

Scenario 3: Alex (Mixed Mode, GBP 3,000/month, 40% International)

Setup:

- Gold tier (5% portfolio in NEXO)

- Toggles between Credit (large purchases) and Debit (daily spending)

- GBP 5,000 idle balance for APY

- $5,000+ balance - qualifies for cashback

Monthly math:

- Rewards: GBP 3,000 x 1.0% = GBP 30 in NEXO

- APY on GBP 5K: up to 14% APY (rate varies by tier and asset; at Gold tier, yield adds meaningfully to card returns)

- FX fees (40% intl, mixed weekday/weekend): GBP 1,200 x 0.35% avg = -GBP 4.20

- Credit APR cost (on GBP 1,500 credit spend): GBP 1,500 x 3.9% / 12 = -GBP 4.88

- Net monthly value: GBP 30 cashback minus fees plus daily yield on idle balance

His verdict: "Credit mode for big purchases keeps my BTC untouched. Debit mode for groceries. The toggle is genuinely useful. But Gold's 3.9% APR means credit mode costs almost as much as the 1.0% cashback earns. I would need Platinum to make credit mode clearly profitable."

Lesson: Nexo's value scales with tier. Base and Silver are underwhelming. Gold barely breaks even on credit mode. Only Platinum (2% cashback, 1.9% APR) generates meaningful net value from the credit/debit combination.

Spending and ATM Limits

| Limit | Amount |

|---|---|

| Monthly spending | $20,000 |

| ATM daily limit | $1,000 |

| Free ATM per month | EUR 200-2,000 (tier-dependent) |

| ATM over-limit fee | 2% (min EUR/GBP 1.99) |

| Credit line (50% LTV) | Up to 50% of collateral value |

Availability

- Regions: EEA, UK, and Switzerland

- Not available: US, LATAM, APAC, Middle East, Africa

- KYC: Full verification required

- Virtual card: $50 minimum balance to activate

- Physical card: Ordering paused since January 2025

Supported Collateral Assets (Credit Mode)

BTC, ETH, USDT, USDC, NEXO, and 40+ other assets. BTC and ETH have the highest LTV allowance and the lowest APR (Low-Cost rates at Gold/Platinum with LTV below 20%).

2026 Regulatory Status

Licensing:

- Nexo operates through multiple EU-licensed entities

- Regulated in Bulgaria (Nexo Financial LLC)

- MiCA compliance in progress

- Previously faced regulatory challenges in the US (settled with SEC in January 2023 over its Earn product)

Card issuance:

- Card network: Mastercard

- Custody: Hybrid (fiat in regulated accounts, crypto on Nexo platform)

- Operating since 2018, $8B+ in assets under management

What is protected:

- Fiat balances in Debit mode (held in segregated accounts per EU electronic money regulations)

- Card transactions under Mastercard's dispute resolution

What is NOT protected:

- Your crypto used as collateral in Credit mode (liquidation risk is yours)

- NEXO token value (volatile, subject to market conditions)

- Yield on idle balances (platform-managed, not insured)

- Credit mode loans (if Nexo fails during an active loan, collateral recovery is uncertain)

What Happens If Nexo Fails?

Your fiat balance (Debit Mode):

- Held in segregated accounts at regulated banks

- Protected under EU electronic money regulations

- Expected recovery: 90-100% within 30-90 days

Your crypto on Nexo:

- Nexo maintains insurance on custodial assets via BitGo and Ledger Vault

- In bankruptcy, crypto holders are unsecured creditors

- Nexo's lending and borrowing activities add counterparty risk beyond simple custody

Your active Credit Mode loans:

- This is the critical risk. If Nexo fails while you have an active loan:

- Your collateral is locked on their platform

- Bankruptcy proceedings could freeze collateral for months or years

- You might owe the loan amount but lose access to collateral

- Historical comparison: Celsius users with active loans faced 18+ months of uncertainty

Your NEXO tokens:

- Would likely lose 90%+ of value if the platform fails

- This compounds losses for high-tier users who hold 5-10% in NEXO

Mitigation strategy:

- Keep Credit mode borrowing to amounts you could repay if collateral is frozen

- Never hold more NEXO tokens than needed for your target tier

- Convert NEXO cashback rewards to BTC/ETH regularly and withdraw to self-custody

- Use Debit mode for most spending; reserve Credit mode for tax-strategic large purchases

Nexo stability indicators (2026):

- Operating since 2018 (8 years)

- Insurance on custodial assets via BitGo and Ledger Vault

- $8B+ in assets under management

- SEC settlement completed (2023)

- MiCA compliance in progress

- No major security breaches

How Nexo Compares: Head-to-Head

| Feature | Nexo | Crypto.com | Plutus | Kraken |

|---|---|---|---|---|

| Credit Mode | Yes (1.9-13.9% APR) | No | No | No |

| Max Cashback | 2% NEXO / 0.5% BTC | 8% in CRO | 9% in PLU | 1% in BTC/EUR |

| Cashback Minimum | $5,000 balance | None | None | None |

| Token Requirement | 10% portfolio in NEXO | $500-$1M CRO stake | PLU stacking | None |

| APY on Idle | Up to 14% | 0% | 0% | 0% |

| FX Fee (EEA) | 0.2% weekday / 0.7% weekend | 0% | 0% (paid tier) / 2.5% (free) | 0% |

| Annual Fee | $0 | $0 (free tier) | $0-$16.99/mo | $0 |

| Regions | EEA, UK, CH | Global (95+) | UK, EEA | EEA, UK |

| Best For | Tax-efficient HODLers | Lifestyle + global | UK/EU perk maximizers | Zero-fee simplicity |

Nexo wins on:

- Only card with instant Credit/Debit toggle (unique in the market)

- Tax efficiency in high-tax jurisdictions (Germany, France, UK) - borrowing is not a taxable event

- Up to 14% APY on idle debit balances (highest yield-on-card in the market)

- No staking lockup (hold NEXO, do not stake it - sell anytime, though tier drops)

- ZiC structured borrowing at 0% for BTC/ETH holders (separate feature with collar terms)

Nexo loses on:

- Lower reward ceiling (2% max vs 4-9% for competitors)

- Requires $5,000 minimum balance for ANY cashback

- FX fees on every transaction (0.2-2.5% vs 0% for Crypto.com and Kraken)

- Requires holding volatile NEXO tokens for best rates

- EEA/UK/CH only (no US, no APAC, no LATAM)

- Credit mode APR makes borrowing unprofitable below Platinum tier

- Physical card ordering paused since January 2025

Is the Nexo Dual Card Worth It in 2026?

Use the Nexo Dual Card if:

- You hold significant crypto (BTC/ETH) and want to spend without selling or triggering capital gains tax

- Your account balance exceeds $5,000 (otherwise zero cashback)

- You can reach Platinum tier (10% portfolio in NEXO) to unlock the 1.9% APR credit line

- You understand margin risk and can maintain conservative LTV ratios during market downturns

- You are in the EEA, UK, or Switzerland and value flexible spending modes

- You live in a high capital gains tax jurisdiction where borrowing-based spending saves thousands

Skip the Nexo Dual Card if:

- You cannot reach Platinum tier. Below Platinum, the Credit mode APR (3.9-13.9%) costs more than the cashback earns. Use Krak Mastercard or Gnosis Pay instead

- Your account balance is under $5,000. You get zero cashback. Use Kraken for 1% with no minimum

- You want maximum cashback. Nexo caps at 2%, while Plutus offers 3-9% and Crypto.com offers up to 8%

- You want zero FX fees. Nexo charges 0.2%+ on every international purchase. Crypto.com and Kraken offer 0%

- You want self-custody. Nexo is hybrid custodial. Gnosis Pay or Ready offer self-custodial spending

- You are uncomfortable with NEXO token concentration risk. 10% of your portfolio in a platform token is significant

- You are in the US, APAC, or LATAM (EEA, UK, and Switzerland only)

Final verdict: The Nexo Dual Card is the most sophisticated crypto card for tax-conscious European investors with $20K+ in crypto. The Credit/Debit toggle is genuinely unique - no other card lets you instantly switch between spending your balance and borrowing against your portfolio. For a Platinum-tier user spending EUR 4,000/month, the combination of 2% cashback in Credit mode, 1.9% APR borrowing, and tax-deferred spending generates approx. EUR 855/year in net value (before tax savings). But the card demands sophistication: $5,000 minimum for any rewards, NEXO token exposure for tier benefits, 0.2%+ FX on every purchase, and the complexity of managing a lending-backed card. Below Platinum, the economics do not work for Credit mode - use Debit mode for up to 14% APY on idle balances, or choose a simpler card entirely.

Fees and ROI framework

$0 annual fee. FX: 0.2% weekday / 0.7% weekend (EEA/UK/CH), 2% / 2.5% (ROW) - no tier-based reduction. ATM: free up to EUR 200-2,000/month by tier, then 2% (min EUR/GBP 1.99). Credit APR: 1.9% (Platinum, LTV below 20%) to 13.9% (Base). Cashback requires $5,000 minimum balance. Rewards: 0.5% NEXO / 0.1% BTC (Base) to 2.0% NEXO / 0.5% BTC (Platinum, 10% portfolio in NEXO). Credit mode loan repayment: 0.26% fee on crypto (stablecoin repayments free). At Platinum with EUR 3,000/month domestic spend in Credit mode: EUR 720/year cashback minus EUR 684 APR cost = EUR 36 net from card alone. Adding up to 14% APY (tier-dependent) on idle balance significantly boosts total returns. The true cost is NEXO token exposure - a 30% NEXO price drop on a $5,000 holding wipes out more than a year of net card value. ZiC (Zero-Interest Credit) is a separate collar product for BTC/ETH with 0% interest but capped upside.

Competitor comparison

- vs Crypto.com: Crypto.com offers 2-8% CRO with staking ($500-$1M). Nexo offers 0.5-2% NEXO with portfolio allocation (no lockup). Crypto.com wins on max rewards, lifestyle perks (lounge, rebates), global availability, and 0% FX. Nexo wins on credit mode (tax efficiency), up to 14% APY on idle balances, and no staking lockup.

- vs Plutus: Plutus offers 3-9% PLU with subscription + stacking (UK/EEA). Both reward in native tokens. Plutus wins on max rewards and subscription rebates. Nexo wins on credit mode, up to 14% APY on idle balances, and no subscription fee.

- vs Kraken: Kraken offers 1% in BTC/EUR with zero fees, zero token requirement, no minimum balance. Kraken wins on simplicity, 0% FX, and accessibility. Nexo wins on credit mode and higher max cashback (2% vs 1%).

Availability and compliance notes

EEA (30 countries), UK, and Switzerland. Not available in US, APAC, or LATAM. Standard KYC required. Loyalty tiers based on NEXO token portfolio percentage (0-10%). Virtual card requires $50 minimum balance. Physical card ordering paused since January 2025 (requires $5,000 + Gold tier when available). Card currency EUR or GBP, chosen once at activation. Mastercard network. Apple Pay and Google Pay supported. Insurance on custodial assets via BitGo and Ledger Vault. MiCA compliance in progress. Credit mode loan repayment: 0.26% fee on crypto repayments (stablecoins exempt).

Sources and Verification

FAQ

How do you choose Nexo Dual Card crypto cards?

We compare verified issuer sources, fees, and eligibility. Availability can change, so confirm with the issuer before applying.

Do all cards in this list offer the same benefits?

No. Each issuer defines its own program terms. Review the sources on each card profile.

Are these rankings or recommendations?

No. Lists are filtered views of cards in our database and do not imply rankings.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?

User Reviews

Reviews are moderated and may take a moment to appear.

Recent Updates to Nexo Dual Card

- Corrected cashback logic so rewards are now clearly limited to Credit mode rather than implied in Debit mode

- Kept the verdict centered on tax-efficient borrowing and flexible mode-switching instead of generic cashback